On 15 April 2021, the Biden administration imposed new sanctions on Russia in response to (1) its efforts to interfere in U.S. and other countries’ elections, (2) the Solar Winds hacks, and (3) Russia’s continued occupation of the Crimea region of Ukraine. These new sanctions include broad authority under a newly issued Executive Order to impose sanctions across any sector of the Russian economy, including asset freezes, additional targeted designations, and visa restrictions (the new Executive Order, or EO).

The administration concurrently issued a new directive that prohibits U.S. financial institutions from trading in both certain non-ruble and ruble-denominated Russian sovereign debt on primary markets. The new sanctions expand existing restrictions on trading in Russian non-ruble-denominated debt by U.S. banks. Finally, the Office of Foreign Assets Control (OFAC) at the U.S. Department of the Treasury used the new and existing Executive Orders to designate more than 40 individuals and entities.

Summary

- The new Executive Order, “Blocking Property with Respect to Specified Harmful Foreign Activities of the Government of the Russian Federation,”1 provides broad authority to designate anyone operating in the technology or defense sectors of Russia, or any other sector of the Russian economy as identified by the Treasury Department. The EO signals that anyone engaged in Russia-related activities should carefully evaluate the risks of doing so, as further rounds of designations may follow targeting a wide range of sectors of the Russian economy. OFAC has previously used the similarly broad designation authority in connection with the sanctions program against Venezuela, when it simultaneously identified targeted sectors of its economy such as energy and designated persons operating in them such as PdVSA, the state-owned energy company.

- The new sovereign debt restrictions expand upon prior restrictions and now prohibit U.S. financial institutions from participating in both ruble and non-ruble-denominated debt after 14 June 2021. This prohibition builds on existing prohibitions imposed on Russia following its use of chemical weapons in an attempted assassination in the United Kingdom in 2019. These new prohibitions only apply to participation in primary, not secondary markets. These restrictions may also be expanded to include trading on secondary markets should relations with Russia deteriorate further.

- The worldwide scope of the targets sanctioned by OFAC in three separate, concurrent actions further indicates that the United States will continue to target Russian actors engaging in destabilizing activities wherever they are found. The new designations focus on Russia’s expansive disinformation and political interference campaigns in the United States and Africa, as well as Pakistani enablers of such campaigns, Russia-linked cyber attacks such as the Solar Winds attack, and persons that continue to assist in Russian occupation of Crimea. The EO and accompanying designations also identified specific digital currency addresses used by certain of these sanctions targets, emphasizing the increased focus by OFAC on the use of digital currencies and assets in illicit activities.

- Whether the situation escalates and the United States imposes additional sanctions will likely depend on the Russian response and evolution of the U.S.-Russia relationship. In his statement accompanying the sanctions, President Biden noted that he did not want to start a new cycle of escalation and conflict with Russia but chose instead to impose new sanctions that he deemed proportional to Russia’s continued destabilizing activities. However, the President made clear that he will continue to impose costs for Russian government actions that harm the United States.2

The New Executive Order

With the expansive sanctions authorities granted in the new Executive Order, the Biden administration is signaling that it is willing to respond to a wide range of Russian malign activity, regardless of its geographic scope. Such a sanctions approach may create challenges for companies trying to assess potential sanctions designation risk of their customers and counterparties. These new targeting authorities include:

- Providing the Secretary of the Treasury with the authority to designate and freeze the assets of any person operating in any identified sector of the Russian economy. While the Executive Order identifies only the technology and defense sectors as targets, it expressly authorizes the Secretary of the Treasury to identify any additional economic sector and freeze the assets of any person operating in that sector. This broad discretion increases the risk for companies operating in Russia, as their customers or counterparties could be at risk for designation. However, it remains to be seen how OFAC may use this authority. For example, Executive Order 13662 was structured in a similar way and authorized imposition of blocking sanctions, but the Obama Administration chose a more targeted, sectoral sanctions approach to avoid broader, negative consequences stemming from a designation of a major Russian bank or company. The Biden administration could similarly apply a range of sanctions with future designated sectors, including additional debt/equity/lending restrictions, or broader assets freezes.

- Creating new sanctions targeting authorities for a wide range of illicit Russian activity. These include helping the Russian Government engage in malicious cyber-enabled activities, actions or policies that undermine democratic processes and institutions in the United States or abroad, transnational corruption, or assassination and murder. In addition, the EO provides authority to target any person that helps the Government of Russia engage in deceptive or structured transactions designed to circumvent U.S sanctions, including through the use of digital currencies or assets.

- Authorizing OFAC to designate spouses and adult children of persons designated under the Executive Order. This is likely in response to multiple press reports on how Russian government officials and oligarchs avoid U.S. sanctions by transferring their wealth to family members. This designation authority may create significant compliance challenges, particularly in situations where the relationship between a designated person and his or her spouse or adult children is not evident.

New Sovereign Debt Restrictions

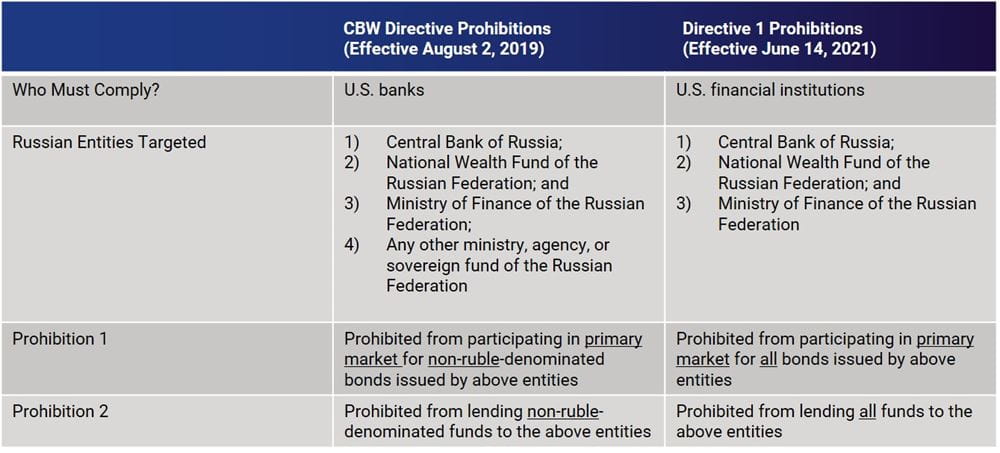

- OFAC also issued Directive 13 and four related OFAC Frequently Asked Questions (FAQs) to implement new Russian sovereign debt restrictions pursuant to the new Executive Order.4 This new Directive adds restrictions on ruble-denominated Russian sovereign debt to ongoing restrictions with respect to non-ruble-denominated Russian sovereign debt. Directive 1 specifically targets debt issued by three Russian Federation entities: (1) the Central Bank of the Russian Federation, (2) the National Wealth Fund of the Russian Federation, and (3) the Ministry of Finance of the Russian Federation (Directive 1 Entities).

- Directive 1 generally prohibits “U.S. financial institutions” from engaging in two activities beginning on 14 June 2021: (1) participation in the primary market for ruble- or non-ruble-denominated bonds issued by the Directive 1 Entities; and (2) lending ruble- or non-ruble-denominated funds to the Directive 1 Entities. Directive 1 broadens the prohibitions contained in the Chemical and Biological Weapons (CBW) Directive issued in August 2019.5 The CBW Directive prohibits “U.S. banks” from participating in the primary market for non-ruble-denominated bonds issued by and lending non-ruble-denominated funds to Russian Federation entities. Directive 1 extends this prohibition further by restricting “U.S. financial institutions” from participating in the primary market for non-ruble-denominated bonds to all bonds traded on the primary market by the three Directive 1 Entities, and by prohibiting the lending of all funds to those entities, regardless of denomination.

- U.S. financial institutions can still participate in the secondary market for bonds issued by the Directive 1 Entities after 14 June 2021. FAQ 889 clarifies that Directive 1 does not prohibit U.S. financial institutions from participating in the secondary market for bonds issued by the Directive 1 Entities. This application of the prohibition only to primary markets will likely limit its impact. This restricted application was likely intentional; the Biden administration wanted to increase sanctions pressure on Russia but not take steps—such as targeting secondary markets—that could be seen as too escalatory.

- The burden of complying with Directive 1 largely falls on the same U.S. companies as the CBW Directive. Under Directive 1, the definition of “U.S. financial institutions” is slightly broader than the definition of “U.S. bank” under the CBW Directive. Notably, the CBW Directive applies to “commodity futures and options brokers and dealers” (emphasis added), whereas Directive 1 applies to all “futures and options brokers and dealers.” Other than that difference, the definitions are largely the same.

- OFAC’s 50 percent rule does not apply to the entities listed in Directive 1. FAQ 891 clarifies that OFAC’s 50 percent rule does not apply to Directive 1. This means that the prohibitions do not apply to any entity owned, directly or indirectly, 50 percent or more by one or more of the Directive 1 Entities, whether individually or in the aggregate. This approach stands in contrast to OFAC’s position on Specially Designated Nationals (SDNs) and Sectoral Sanctions Identifications (SSI) entities, where the 50 percent rule does apply. This clarification should make it easier for financial institutions to conduct due diligence and ensure they are not participating in ruble- or non-ruble denominated sovereign debt in primary markets.

15 April 2021 OFAC Designations

The Treasury Department also took action against more than 40 individuals and entities for a range of malign activity, including Russia’s attempts to interfere with elections, continued operations in Crimea, and sanctions evasion. These entities were already sanctioned under a range of Executive Orders and some are also subject to prohibitions under the Countering America’s Adversaries Through Sanctions Act of 2017, meaning Congress would have to approve their removal from the SDN List.

- Actions taken under the new Executive Order target the technology sector in Russia. 16 companies and 16 individuals were designated for operating in the technology sector of the Russian economy. For example, one of the sanctioned entities, SouthFront, is an online disinformation site registered in Russia that receives taskings from the Federal Security Service (FSB). In the aftermath of the 2020 U.S. presidential election, SouthFront sought to promote perceptions of voter fraud by publishing content alleging that such activity took place during the 2020 U.S. presidential election cycle. U.S. persons doing business with Russian firms in the technology sector should ensure that they conduct proper due diligence on their customers or counterparties and assess whether designation risk may exist.

- If the Russian government continues to spread misinformation to influence U.S. and other countries’ elections, the Biden administration will likely continue to target propaganda outlets controlled by the Russian government. Several individuals and entities were designated for their continued support to or operations on behalf of previously designated Yevgeniy Prigozhin, a Russian financier of the Internet Research Agency (IRA). For example, the Association for Free Research and International Cooperation (AFRIC) was designated for serving as a front company for Prigozhin’s influence operations in Africa, including sponsoring phony election monitoring missions in Zimbabwe, Madagascar, the Democratic Republic of the Congo, South Africa, and Mozambique. The Treasury Department will likely continue targeting entities engaged in election interference.

- Future sanctions actions will likely highlight the use of digital currency to abuse the international financial system. OFAC also targeted Pakistan-based Second Eye Solution (SES) for assisting the IRA in concealing its identity to evade sanctions. OFAC also identified multiple digital currency addresses used by SES to fulfill customer orders.

- The sanctions actions against individuals and entities related to the Russian occupation of Crimea suggest that the United States is working to align certain elements of its Russia sanctions program with international allies. As part of an effort to pressure Russia over its continued occupation of Crimea, the United States sanctioned a number of persons, including some who were already designated by the European Union, the United Kingdom, Canada, and Australia.

Implications for the Private Sector

- The broad sanctions authorities under the new Executive Order place a spotlight on the evolving U.S.-Russia relationship and the potential for additional sanctions. The administration’s actions appear designed to seek to deter malign Russian activity and to disrupt specific networks and operations. In light of President Biden’s stated intention to impose additional costs on Russia, companies should evaluate their exposure to Russian companies operating in the technology, defense, and cyber sectors, as well as Russian state-owned enterprises or companies owned and operated by Russian government officials.

- Both U.S. and non-U.S. market participants should evaluate their exposure to Russian sovereign debt and their risk appetite for participating in secondary markets for Russian sovereign debt. While the compliance burden in implementing Directive 1 is likely to be light given existing CBW Directive prohibitions on transacting in non-ruble-denominated debt on primary markets, the evolving U.S.-Russia relationship may result in expanded sanctions and restrictions related to Russian sovereign debt. For example, should Russia retaliate or escalate the situation in Ukraine, the administration may choose to impose restrictions on trading in secondary markets on Russian sovereign debt.

- Financial institutions that provide services to spouses or adult children of senior Russian government officials or individuals working closely with or linked to the Russian government should undertake additional due diligence to assess sanctions designation risk. The Treasury Department has previously sanctioned Russian oligarchs’ children for setting up front companies or storing separate funds in their family member’s accounts. Given the new Executive Order’s authority to target spouses or adult children of a range of Russian individuals, financial institutions should ensure to the extent possible that any customers who are close family members of Russian government officials or otherwise closely linked to the Russian government are not using accounts or services on behalf of these family members.

- Companies engaged in the information and communications technology and services (ICTS) sector should also consider administration action to limit transactions involving Russian ICTS companies. The Solar Winds hack demonstrated the risks posed by Russia’s efforts to target companies worldwide through supply chain exploitation. The administration highlighted the risks of using ICTS supplied by companies that operate or store user data in Russia or rely on software development or remote technical support by personnel in Russia. The U.S. government is reportedly evaluating whether to take action under Executive Order 13873 to better protect the U.S. ICTS supply chain from further exploitation by Russia.6

- The new Executive Order also increases sanctions risks related to energy supplies and pipelines. While Nord Stream 2 targets were not designated as part of the 15 April action, the new Executive Order provides authority to target any person responsible for or complicit in cutting or disrupting energy supplies to Europe, the Caucasus, or Asia. While the Biden administration continues to try to stop the Nord Stream 2 project through direct sanctions pressure tied to that project, the new sanctions authorities provide a potential deterrent to Russian action to halt fuel supply to Europe if the pipeline is eventually completed.

Endnotes

1 “Executive Order Blocking Property With Respect to Specified Harmful Foreign Activities of the Government of the Russian Federation” (April 15, 2021), available at https://home.treasury.gov/system/files/126/russian_harmful_for_act_eo.pdf.

2 “Fact Sheet: Imposing Costs for Harmful Foreign Activities by the Russian Government” (April 15, 2021), available at https://www.whitehouse.gov/briefing-room/statements-releases/2021/04/15/fact-sheet-imposing-costs-for-harmful-foreign-activities-by-the-russian-government/.

3 “Directive 1 Under Executive Order of April 15, 2021 Blocking Property With Respect to Specified Harmful Foreign Activities of the Government of the Russian Federation” (April 15, 2021), available at https://home.treasury.gov/system/files/126/sovereign_debt_prohibition_directive_1.pdf.

4 “Ukraine-Russia Related Sanctions Frequently Asked Questions.” Available at U.S. Department of the Treasury.

5 See “Executive Order 13883, Administration of Proliferation Sanctions and Amendment of Executive Order 12851” (August 1, 2019), available at https://home.treasury.gov/system/files/126/13883.pdf. The CBW Directive is available at https://home.treasury.gov/system/files/126/fr84_48704.pdf.

6 Executive Order 13873 is designed to create a framework to prohibit, mitigate, or unwind information and communications technology services transactions involving foreign adversaries.